Will the Iran crisis lead to another round of food price spikes?

Agricultural commodity prices have been under sustained downward pressure since 2013–14. The 2022 spike in the wake of COVID-19 disruptions and Russia’s invasion of Ukraine proved temporary rather than cyclical. Now, the Strait of Hormuz closure amid the Iran war has produced a sharp run-up in fertilizer prices, raising agricultural production costs. Yet thus far, global commodities markets have not spiked. More than a month into the crisis, urea prices are up roughly 40%, while wheat and maize prices have increased by about 6% and soybeans less than 3%). Rice prices have fallen over the period.

Are we at the beginning of another period of high food prices? The short answer, in our assessment, is probably not—at least not yet. The conditions that drove prior price spikes are largely absent today, and the Hormuz disruption is a fundamentally different kind of shock than either the 2007-2008 food price crisis or 2022. The Hormuz disruption is a fertilizer supply shock, not a crop supply shock, and that distinction matters both in price formation and appropriate policy responses.

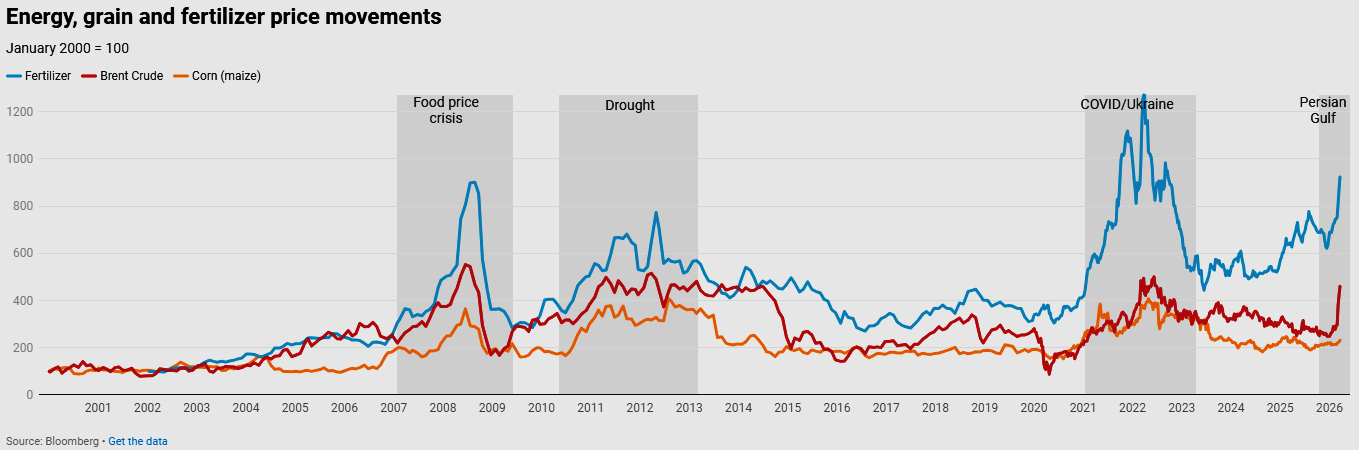

During previous agricultural price spikes, including 2007-2008, 2010-2012, and 2021-2022, energy, fertilizer, and grain prices moved together: rising and falling in tandem (Figure 1). In 2026, the pattern is different: fertilizer and energy prices are rising while grain prices remain roughly flat.

Comparing the Hormuz disruption to the war in Ukraine

The Russia-Ukraine war offers a clear illustration of how the current crisis differs from past food price shocks. Before the February 2022 invasion, Ukraine accounted for roughly 16% of global corn exports and, together with Russia, 29% of wheat exports. The conflict disrupted both grain supply and fertilizer supply from the region simultaneously. Crop prices surged alongside input costs, which partially offset the margin impact for farmers. With maize prices at $235-$275 per metric ton (MT), fertilizer prices at $1,000/MT were costly but manageable.

The Persian Gulf crisis presents a fundamentally different picture. The Gulf states export virtually no grain to the world market. What they do supply is fertilizer—and on a larger scale than Russia and Belarus combined. The Gulf accounts for a significant share of global urea, phosphate, and ammonia trade. Saudi Arabia alone supplies roughly 55% of U.S. ammonium phosphate imports. The major fertilizer producers in Qatar (QAFCO) and Saudi Arabia (SABIC Agri-Nutrients) have declared force majeure and temporarily stopped production of urea.

Iran’s shutdown of most cargo traffic through the Strait of Hormuz has resulted in ships stacked up, awaiting passage that may or may not come anytime soon. As of mid-March, Kpler vessel tracking identified 23 fertilizer vessels loading or laden in the Gulf with transit status uncertain. Nikkei Asia reported 21 ships carrying nearly one million MT of fertilizer were stuck in the Gulf awaiting transit of the Strait.

The 2026 disruption may ultimately prove more severe on the fertilizer side than 2022. Then, Russian fertilizer volumes dipped sharply in the first half of the year before recovering as trade rerouted through Brazil, India, and China. Russian volumes largely recovered by 2023 and reached record levels in 2024. Belarusian potash exports, however, fell by roughly 50% and did not fully recover. In 2026, the physical closure of the strait is a hard constraint: product is manufactured but has no ocean exit. If the strait remains closed and production disrupted for an extended period, fertilizer prices could exceed the 2022 records.

For producers, current maize prices of $155-$165/MT—roughly 40% lower than in 2022—make high diammonium phosphate (DAP) prices of $700/MT-$750/MT far less affordable than they were in 2022. Fertilizer-to-crop price ratios were already at historically poor levels before the Hormuz crisis began. This is the core of the asymmetry: in 2022, high crop revenues helped absorb high input costs. In 2026, that offset does not exist. The deteriorating fertilizer-to-crop price ratio may have potential implications for food production and food security, but at least in the short term, rising food prices are not among them.

See https://www.ifpri.org/blog/will-the-iran-crisis-lead-to-another-round-of-food-price-spikes/

Views: 70